Chemical distribution in Belgium from 2007 to 2010: An empirical study

Abstract

Chemical distribution is described from a product lifecycle perspective. The impact of the economic decline in 2009 on Belgian chemical distribution is given in figures. In 2010 the sector recovered sharply. Although the individual companies performed very differently, overall, 2010 was even better than 2008. Increasingly complex legislation on chemical products has initiated a consolidation trend in the sector which in turn has brought on trends in outsourcing and inventory management.

1 Introduction

Chemical distribution represents a relatively small and unknown sector in Belgium; nonetheless, it provides essential support to many of the Belgian industries. Rather than simply selling chemicals, genuine chemical distributors add value through an extensive range of services to both customers and suppliers. Examples of services offered to customers are product expertise for formulation purposes, Just In Time deliveries, sample management, drumming, dilution and blending transformations. Services offered to suppliers include repackaging, labeling conform local regulations and language and arrangement of import authorizations and new product approvals. Thus chemical distribution originates in the gap between producers who wish to sell large lots without regulatory or logistical complications, and customers demanding small volumes and who have very specific needs on technical, regulatory and logistical level. Modern chemical distributors also provide suppliers with in-depth market intelligence and assist with the implementation of marketing strategies. In essence, chemical distributors allow their principals to profitably reach smaller customers in many industries and countries.

For the purpose of describing chemical distribution, products are commonly classified as either commodity (or industrial) chemicals or specialty chemicals, as these two types differ substantially in traded volumes, pricing mechanism, type of services offered, capital intensity of the business, outsourcing of logistics and applicable regulations on safety and environment. Commodities comprise acids, lyes, solvents, salts and other inorganic products. They are low-value high-volume products for which transport is a major cost factor. Keys to success in commodity markets are therefore competitive pricing, operational excellence and sites located nearby customer centers. Specialties comprise a countless number of products and are best characterized by their industry of application. Keys to success in specialty markets are firstly knowledge of customer needs through regular customer visits, secondly product expertise to relate customer needs to particular products and services and finally flexibility, for example being able to source and deliver on very short notice (Districonsult, October 2010; CHEManager, 2005). Specialty price increases are generally passed on to customers immediately. A more complete description of the sector’s characteristics can for example be found in Districonsult (October 2010), ICIS Chemical Business (May 2010) or CHEManager (2005). Because chemical distribution involves a diverse range of products, and also serving many different industries and working with partners having very different needs, the distributors have very distinguished product portfolios, business models and growth strategies. Together they form a European sector that has changed profoundly over the last decade, see for example CHEManager (2005). More recently European chemical distribution has been impacted visibly by the economic decline in 2009.

2 Objectives, scope, and methodology

The objective of this article is an empirical market study on Belgian chemical distribution. The article summarizes the results of a study carried out for the Belgian Association of Chemical Distributors. The focus is on the following eight firms who are the leading distributors on the Belgian market: Brenntag, Caldic, Univar, Quaron, Azelis, IMCD, Kreglinger and Barentz. These firms are genuine chemical distributors: they work independently of their principals, conduct business mainly through durable distribution contracts (as opposed to trading) and have no production activities of their own. In addition, they have been active in Belgium for at least ten years. The first four firms distribute both commodities and specialties, the other distribute almost exclusively specialties.

Firstly, the study investigates the diversity among the Belgian distributors and provides for this diversity an economic explanation. Secondly, Belgian chemical distribution is represented in figures over the period 2007 – 2010 detailing evolutions in sold volumes, turnover, added value, investment and employment. The main purpose is to assess how the economic decline in 2009 has impacted the Belgian distributors and how they recovered in 2010. Thirdly, the study explores management trends in the sector.

The targeted companies were approached individually to obtain detailed commercial data. In addition, in-depth interviews were held with the Belgian executives from which first-hand information was obtained on business models, management trends and expected future developments in the sector.

3 Company business models: a product lifecycle view

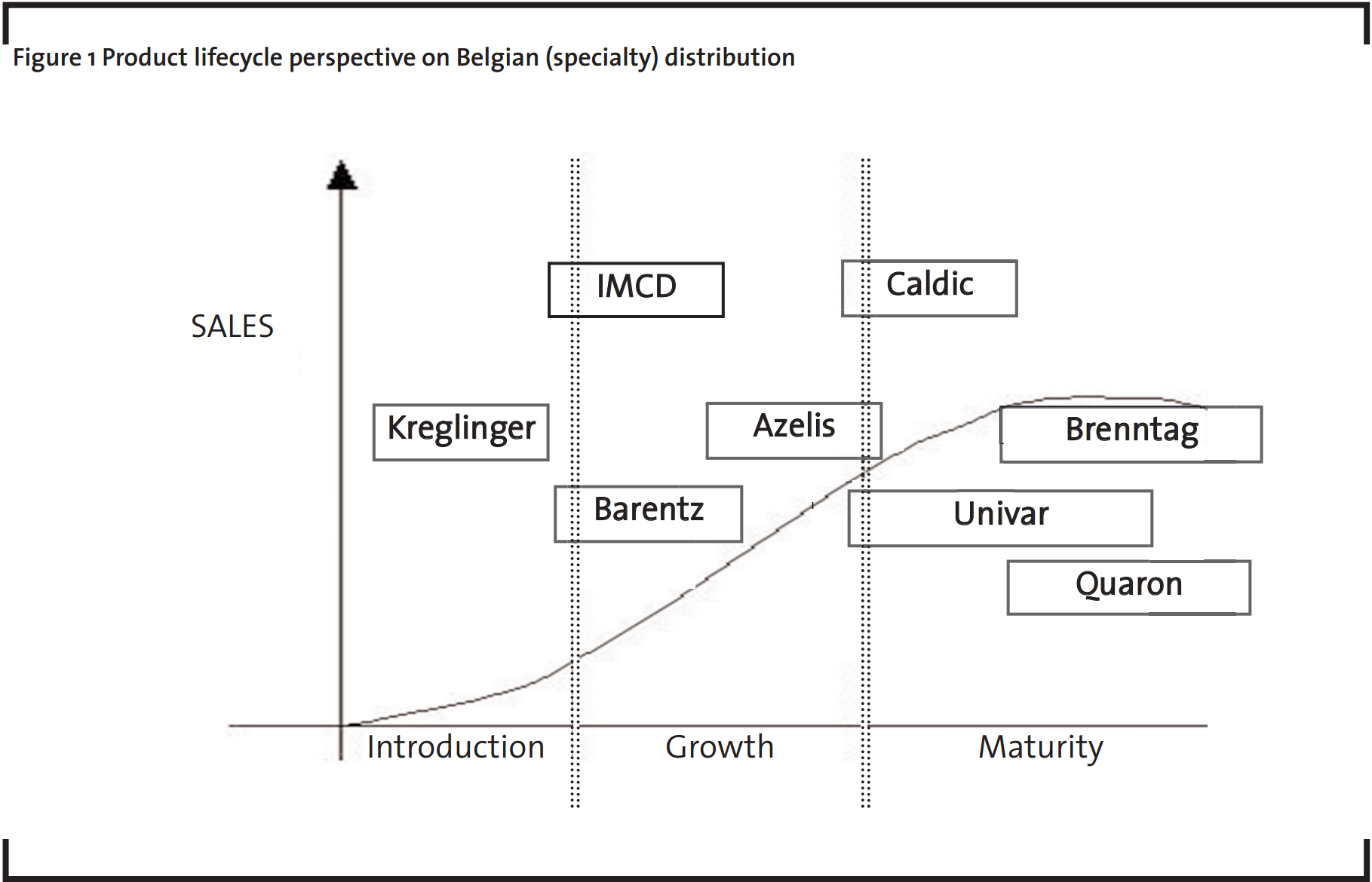

We previously introduced chemical distribution as a very heterogeneous sector. In this section we develop an economic perspective on the sector that allows a description of the heterogeneity. From the interviews the conclusion emerged that the different business models can be related to the phases of the product lifecycle model. As a product proceeds through its lifecycle, the supplier’s needs with regard to distribution will change from phase to phase. For chemical products these changes in needs are so significant that it is difficult to combine them into one distribution company. Thus different distributors exist across lifecycle phases, with business models specifically tailored to supplier’s needs. Elements of the business model include the degree of intimacy and loyalty in the relationship with suppliers, wide or narrow industry focus, offered services, geographic coverage, extent of logistics outsourcing and growth strategy. The product lifecycle view does not capture all possible characteristics of firms, however it provides an economic explanation for many of the observed differences between firms. Figure 1 shows how the eight leading distributors on the Belgian market fit into the product lifecycle view. The positioning in the plot is based on discussions with firms on their business model characteristics and the plot should therefore be interpreted rather qualitatively. Note that the developed perspective is particularly relevant to specialty distribution; commodities are by definition products in the maturity phase.

Products in the ‘Introduction phase’ from Figure 1 are demanded in small volumes by customers from only a few industries, typically the food, cosmetics and pharmaceutical industries. Typical activities in this phase are the dissemination of product documentation to users and the requesting of product approvals from local authorities. The supplier wishes detailed information on users and pricing and expects its distribution partner to implement a defined marketing strategy. Thus the supplier expects from its distribution partner firstly product launching services, secondly extensive feedback on customer profiles and willingness to pay, and thirdly loyalty and exclusivity. Kreglinger is very clearly positioned in the introduction phase. Kreglinger explicitly keeps logistics in-house (excluding transport) because they constitute a key part of their product launching services. Kreglinger explicitly limits its geographical presence to a handful of Western-European countries and works with local home-office salesmen instead of physical subsidiaries. This allows centralized planning and warehousing while maintaining close contact with the user industries. Finally, successfully launching a product may require that customers are provided with some flexibility in payment terms. This is particularly the case for innovators in the cosmetics industry as these customers often depend for their revenue on large conglomerates. Thus distributors in the introduction phase are typically flexible with regard to customer credit.

In the ‘Growth phase’ from Figure 1, the product is finding more applications and innovations based on the product are becoming successful. Hence demand is increasing and returns to scale in production allow prices to decline. Suppliers require a partner who can reach all relevant industries over a large geographic area. Throughout this phase we find Barentz, IMCD and Azelis. These firms still act as loyal marketing partners for their principals, however they do not disclose detailed information on customers and they set prices independently. They each focus on a select number of industries and employ an extensive sales network consisting of physical country subsidiaries. They typically outsource logistics and warehousing completely, as these activities are not key to the selling of products and expertise. Barentz and IMCD differ sharply on aspects like industries of specialization, company size, ownership model and growth strategy. However they are rather similar on aspects that are more relevant to the product lifecycle model: they both specialize in ‘growth-phase products’ for a few industries, offer complete solutions to these industries (e.g. all relevant products and services) and maintain intimate relationships with principals. For this reason, they occupy a similar position in Figure 1. Azelis is positioned more towards the ‘Maturity phase’ because it less values intimacy with principals than the others and has a wider industry focus.

Once a product reaches the ‘Maturity phase’ from Figure 1, the supplier wants to sell large volumes at favorable profit margins. Customer information, marketing services and exclusive relationships are no longer needed. Instead, a distributor must offer operational excellence and wide geographic and industry coverage. All of this is achieved by large company size, offering of multiple brands of the same product and extensive logistics infrastructure. In this phase we find Caldic, Brenntag, Univar and Quaron.

A feature that is not captured in the product lifecycle view, but which is a distinct characteristic of a chemical distributor, is the choice of a firm between autonomy and uniformity of its country subsidiaries. A distributor who operates internationally must constantly balance between, on the one hand, autonomy of subsidiaries to achieve flexibility towards local markets, and on the other hand, uniformity across the organization to benefit from scale efficiencies. To combine these determinants of success, chemical distributors have implemented a matrix organization made up of local country managers and international product managers. Each distributor behaves differently with respect to the above trade-off and this choice is not found to be related to the position in the product lifecycle view.

4 Belgian chemical distribution sector in the crisis: empirical results

The economic decline in 2009 significantly impacted European chemical distribution. The German market turnover and investment volume dropped by 22% and 50% respectively (VCH, 2010). This market is considered to some extent a benchmark for the whole of Europe (ICIS Chemical Business, May 2010). At European level, turnover and traded volumes dropped on average by 15 – 20% and 10 – 15% respectively (Districonsult, March 2010). This implies that prices fell, on average. However the European sector recovered strongly in the first half of 2010 due to a general recovery in industrial activity and due to customers replenishing stocks after having minimized stocks during 2009 (ICIS Chemical Business, October 2010). The purpose of this section is to represent the Belgian sector in figures and to assess how this geographic market has been impacted in 2009. For the assessment of turnover, added value, investment volume and employment we distinguish between all-round distributors (active in both commodities and specialties) and pure specialty distributors to account for the commercial differences between both product types.

4.1 Traded volumes

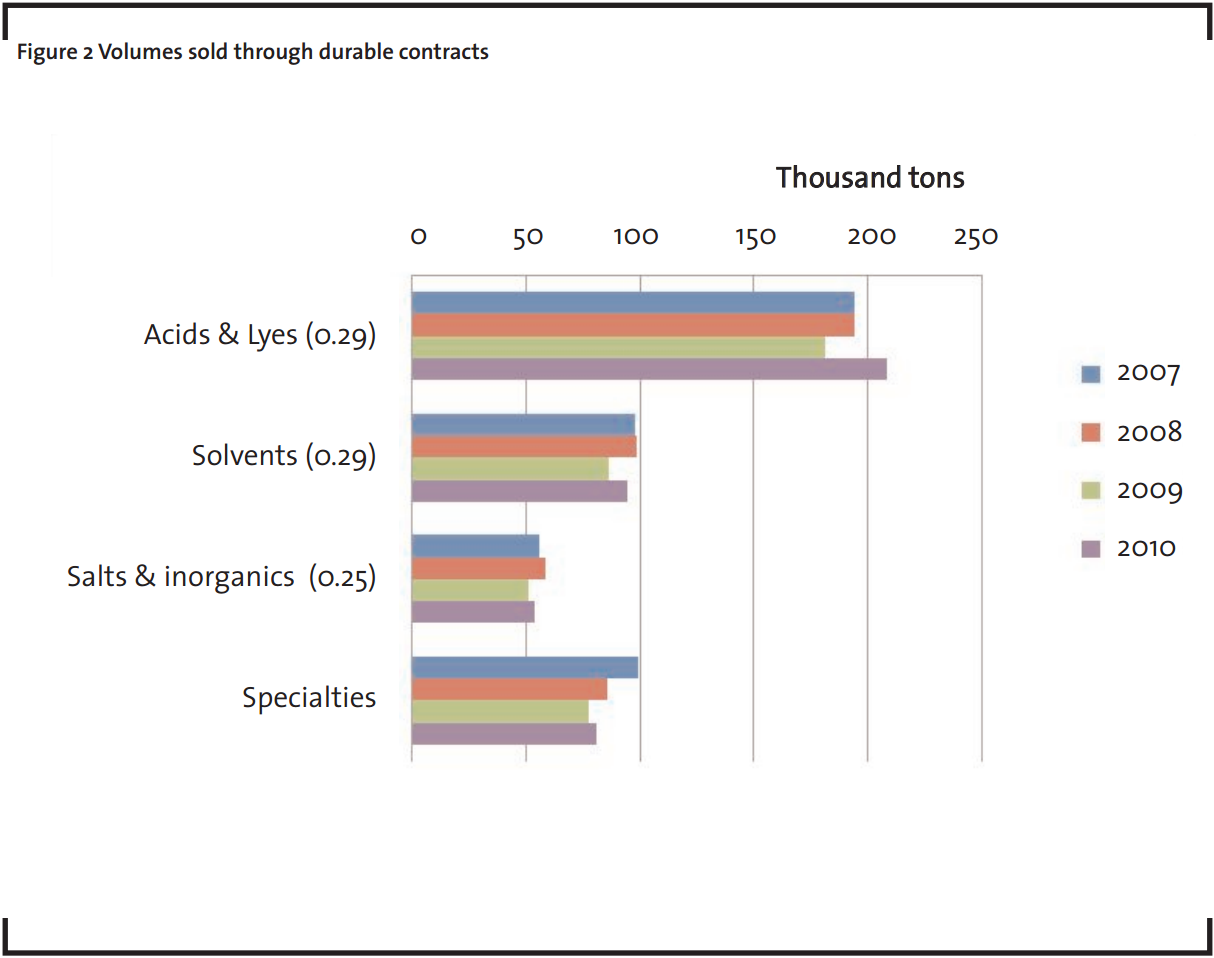

Figure 2 shows evolutions in the volumes sold on the Belgian market by the eight distributors considered in this study. The data represent only sales on the basis of durable distribution contracts. In 2009 total volumes dropped by 6.4, 12.9, 12.3 and 9.2% respectively, corresponding to the order in Figure 2. In 2010 total volumes recovered, however the individual companies performed very differently.

Commodity distribution is for at least 98% in the hands of Brenntag, Caldic, Univar and Quaron. As an indication of concentration in commodity markets the sum of squared market shares 1 for these four firms (volume-based) is given between brackets. In all three markets the concentration indicator remained unchanged over the period considered. However in 2010 Quaron was acquired by competitor Univar, reducing the number of firms in commodity markets from four to three starting from 2011.

4.2 Turnover and added value

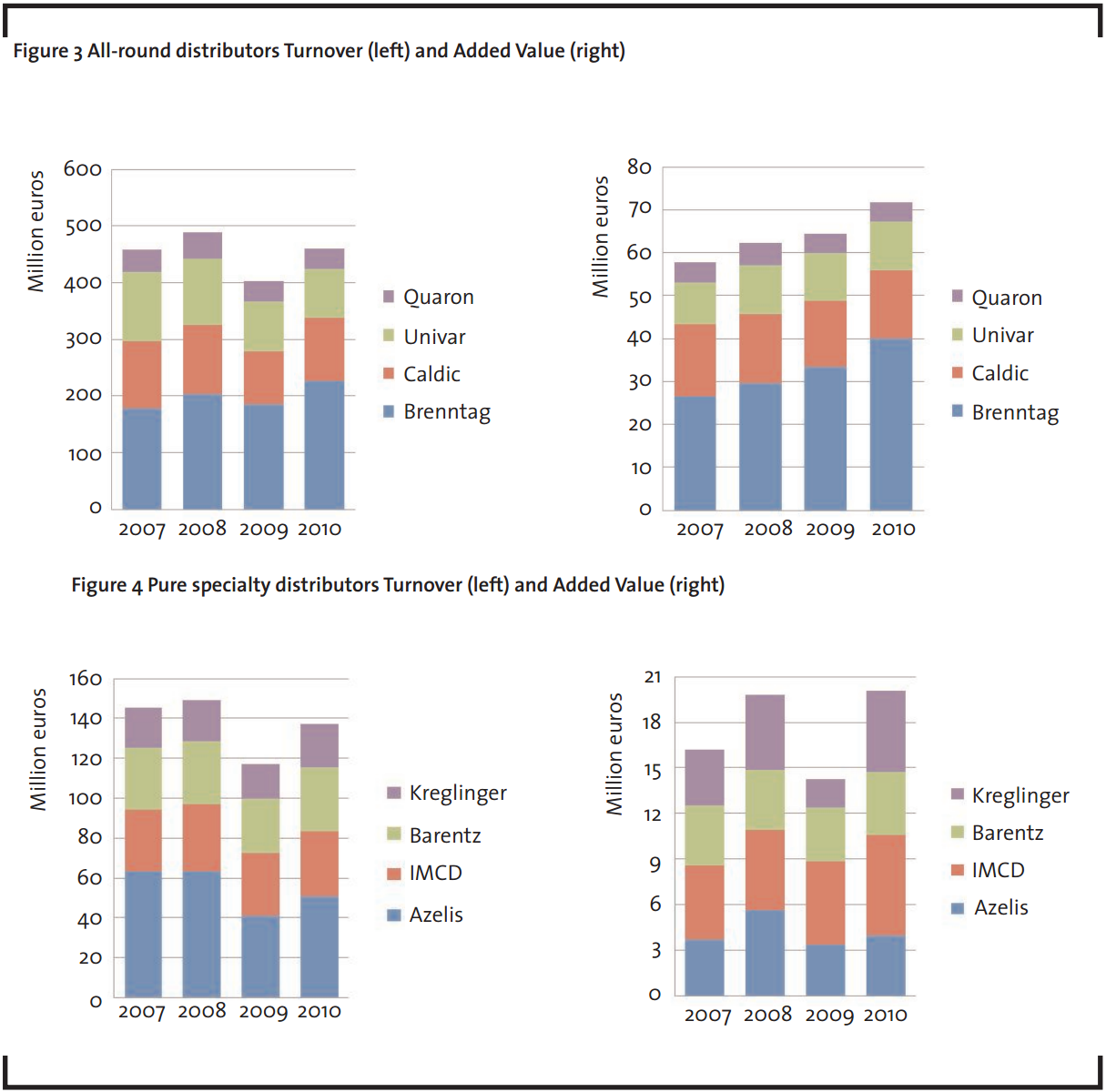

Figures 3 and 4 show, for all-round and pure specialty distributors respectively, evolutions in turnover and added value. Turnover makes a good indicator of the business climate, however chemical distributors focus on added value growth as they strive to offer customers a complete solution rather than just a product. In 2009 the Belgian sector turnover and added value dropped by 18.5 and 4.2% respectively. Although individual performances were very different, the limited decline in added value confirms the view that 2009 was also a year of opportunity as both suppliers and customers were looking for cost efficiencies. For example many customers from the food, cosmetics and paints industries were looking for new formulations with less expensive ingredients, creating opportunities for distributors to promote their product expertise. Moreover, a number of commodities users that were previously serviced directly by suppliers had switched to lower purchasing volumes for which they were referred to the distributors.

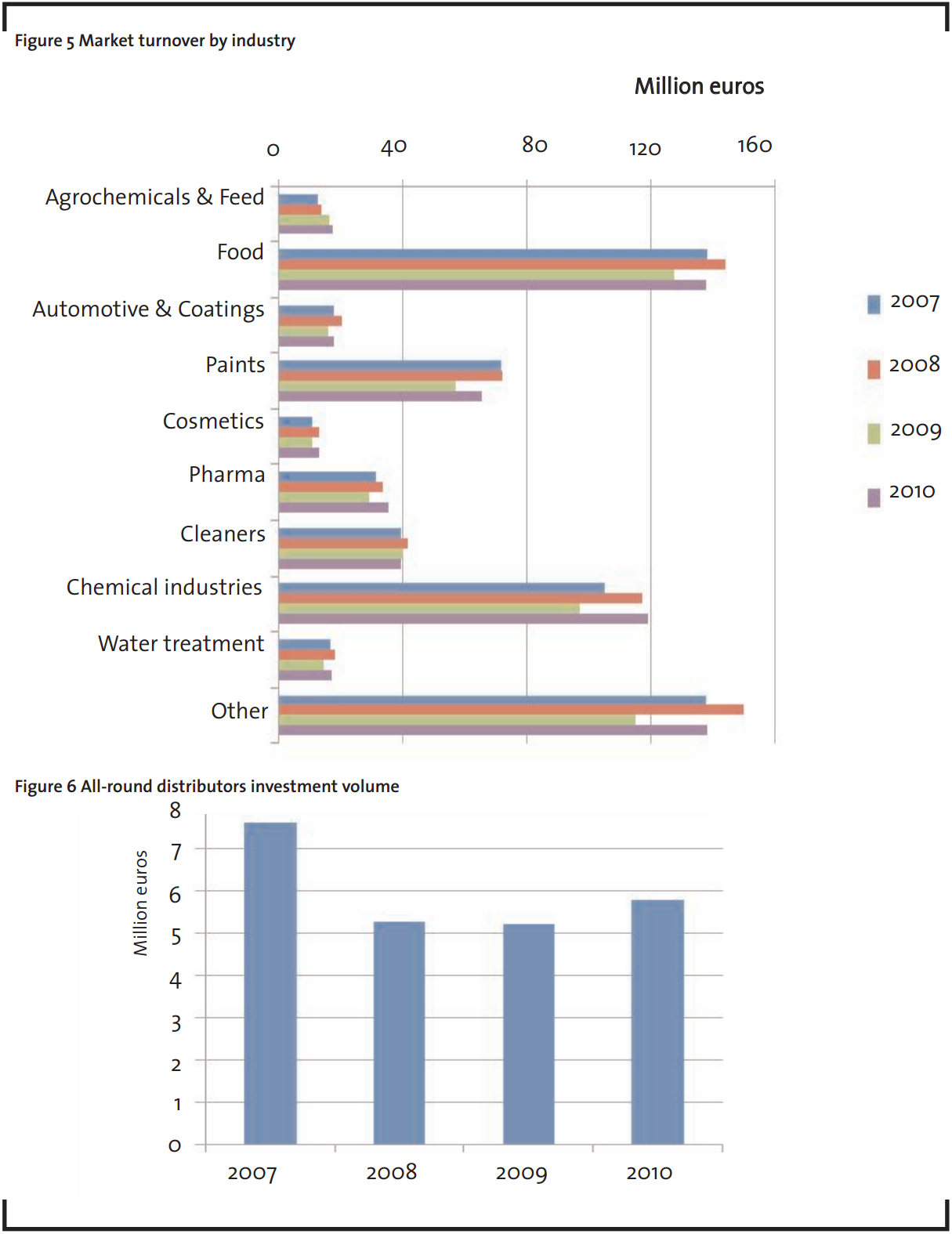

In 2010 Belgian chemical distribution achieved a turnover and added value of 597 and 92 million euros respectively, compared to 638 and 82 million euros in 2008. The key conclusion is that when in 2010 demand for products went up again, distributors benefited from the increased customer awareness and creativity in service development put forth the year before. Figure 5 indicates the share of a range of industries in the sector turnover. The food, paints and chemical industries consistently represent 54% of the Belgian sector turnover. Nearly all industries were severely impacted in 2009. In seven out of the ten industries shown, turnover dropped by more than 15%. The recovery in 2010 is obvious, however only turnover in cosmetics, pharma and chemical industries recovered to the 2008 levels.

4.3 Investment

Total investment volume is almost exclusively attributable to the all-round distributors due to their commodity business. Figure 6 shows the evolution of all-round distributors investment volume. The decline in 2008 was almost completely attributable to one company. The recovery in 2010 was largely attributable to two companies who made exceptional investments in the security of material assets on their sites. Over 2007 – 2010 the ratio of investment volume to added value steadily declined from 13 to 8%. For pure specialty distributors the ratio is consistently lower than 2.5% and represents mostly investments in operational efficiency. For example, distributors increasingly rely on software for management of customer relations and inventory, for reasons to be discussed in Section 5.

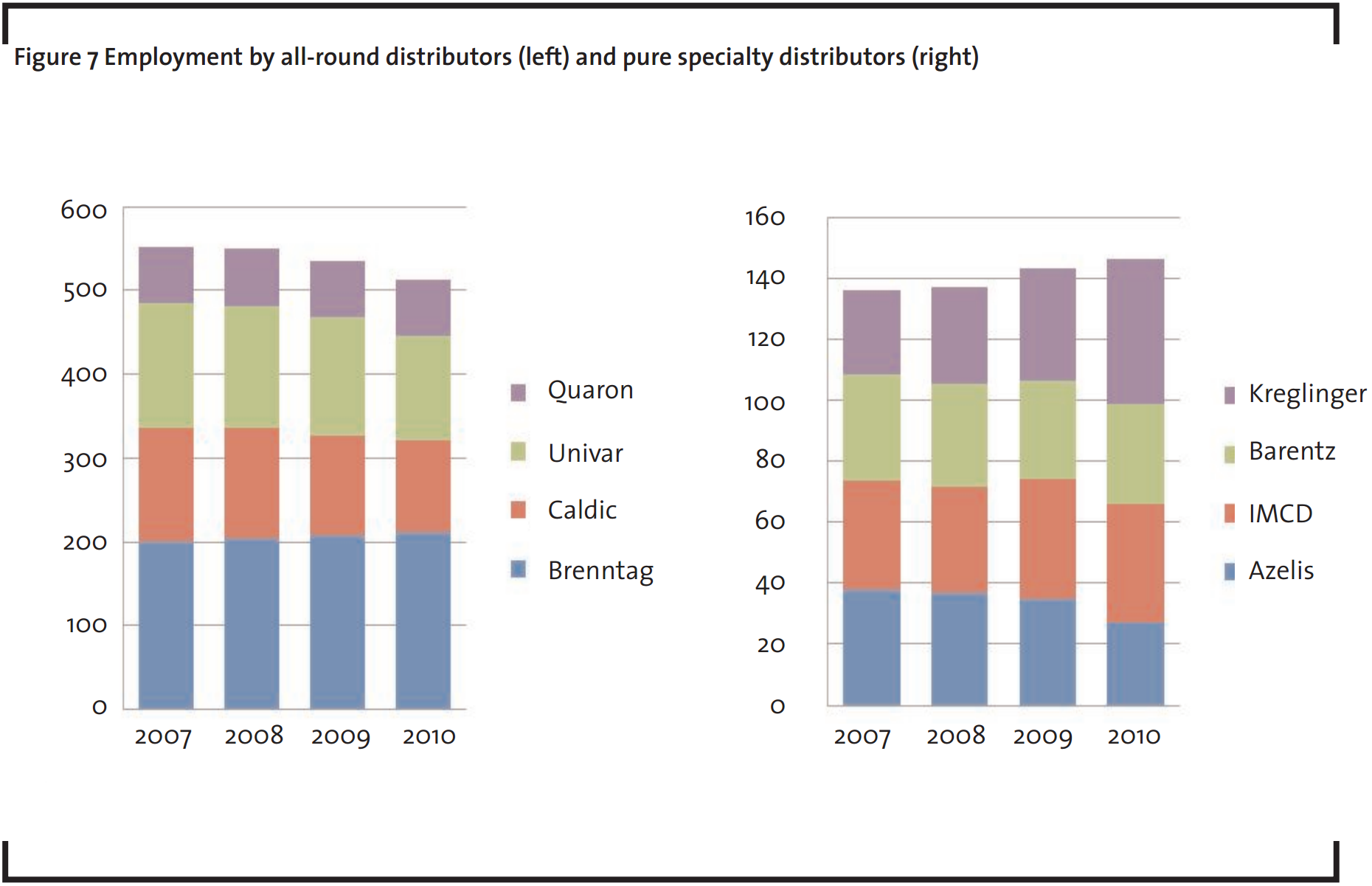

4.4 Employment, labor productivity and labor costs

Evolutions in number of employees are shown in Figure 7. Over 2007 – 2010 total employment in the sector declined slightly from 688 to 677 employees.Different individual evolutions can be seen, however most companies provided a positive outlook for high-skilled labor. Pure specialty distributors typically have a sales force of 35 – 40 employees.

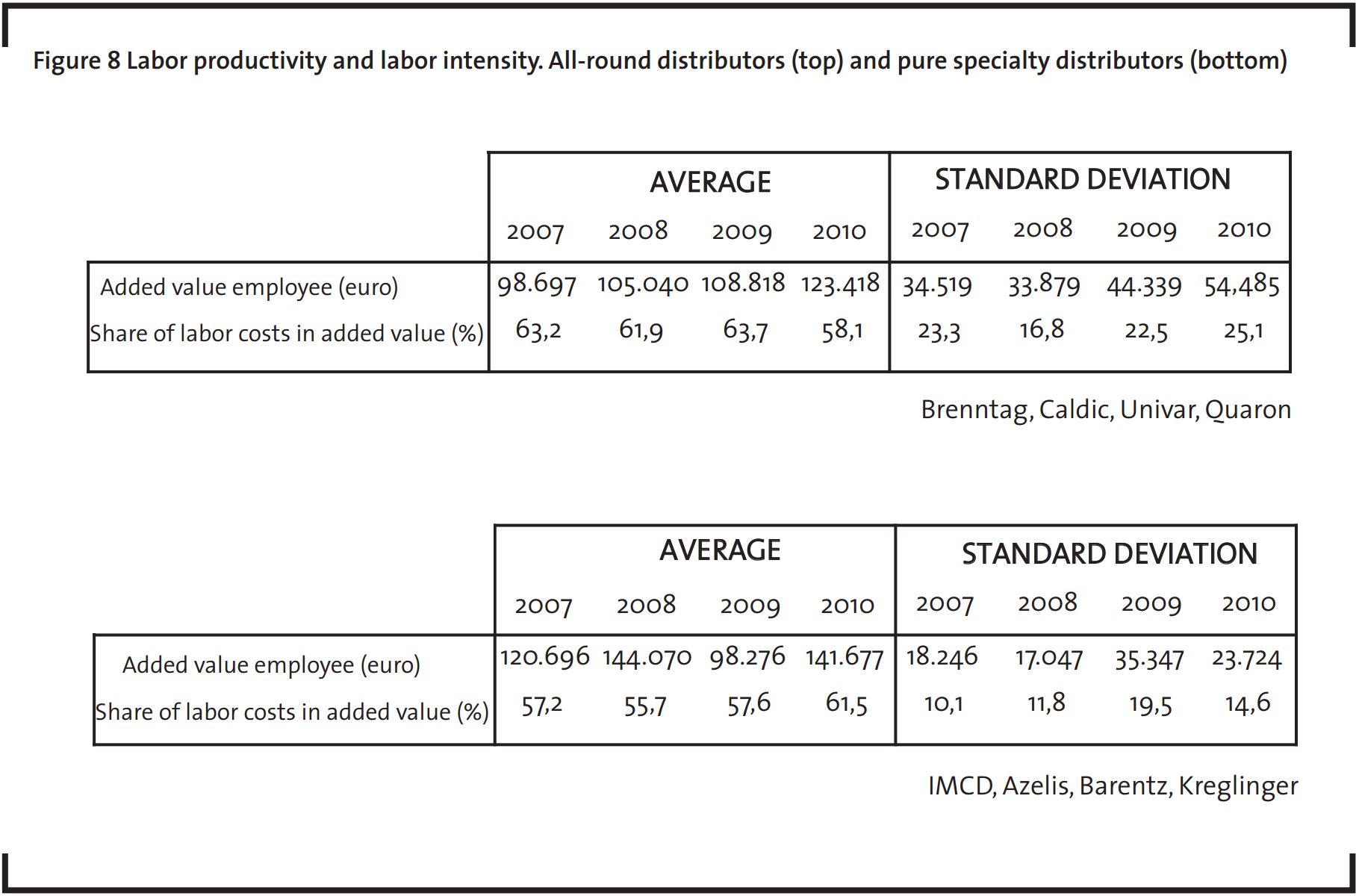

Figure 8 combines the data on added value and employment into an indication of labor productivity and labor intensity in the sector. Significant variability is observed in both labor productivity and labor intensity, which corresponds to the heterogeneity of firms and to the differences in commercial performance over 2007 – 2010.The larger variability is between the all-round distributors because the differences in commercial performance were strongest inthis group. Both indicators show a considerable gap between Brenntag and Caldic on the one hand and Univar and Quaron on the other hand. Moreover, over 2007 – 2010 Brenntag significantly outperformed the others with regard to added value growth.

5 Trends in chemical distribution

In this Section, some remarkable trends within chemical distribution in Belgium are discussed. Chemical distribution is a young sector in development and an overview of its progress during the period 2007-2010 is given.

5.1 Working capital and inventory management

Private equity has since 2005 been very active in chemical distribution and has initiated a trend of rationalization of working capital. Economical use of working capital automatically leads to a focus on inventory management. Forecasting has become an important concept for chemical distributors and more experts are appointed within companies to deal with purchase planning issues. Stocks have decreased and there were less unsold products destructions. In 2010, trade volumes have reached the levels of before the crisis, but a large number of customers are now responsible for smaller, but more frequent orders. Stocks have decreased throughout the chemical supply chain, having a profound impact on the chemical distribution business as distributors are expected to absorb changes in demanded volumes. Hence, inventory management has become an essential part of chemical distribution with respect to competitiveness.

5.2 Impact of REACH

The task of distributors within the REACH regulations is to pass on information between customers and suppliers, for example for the possible application of a product. As a result, the first two phases of REACH, completed in December 2010, increased the number of staff within chemical distributor companies, having to maintain the necessary contacts.

In specialty markets, characterized by small trade volumes, REACH led to some suppliers stepping out of business due to REACH registration costs being too high compared with profitability. The next phases of REACH focus on the smaller chemicals volumes and the supplier effect will therefore become even larger, leading to the risk of monopoly-formation of suppliers (those able and willing to pay the registration costs) for some chemicals.

5.3 2009: year of crisis and opportunities

Belgian chemical distributors indicate that 2009 was a year of crisis as well as of opportunities. Customers and suppliers were in search for increasing their cost efficiencies, leading to the opportunity of distributors to promote new services. Falling prices meant less working capital requirements, hence resources became available to invest in these new opportunities. In 2009, distributors have worked hard to differentiate from their competitors, leading to important positive results in 2010.

The 2009 crisis also pushed towards more economical use of working capital, besides the private equity push on this matter. In 2010, when the market recovered from the economic decline in 2009, the inventory and resources management changes from 2009 were still fully standing, making the chemical distributors to have a strong economic position.

On the one hand, some suppliers did serve themselves certain important customers in 2009, thus bypassing the distributor in the supply chain, and on the other hand, certain customers switched to smaller purchase volumes, and therefore became customer of distributors. In 2009, specialty distributors were mainly confronted with a decreasing demand from the cosmetics industry, and to a much lesser extent a decreasing demand from the food and pharmaceutical industries.

5.4 Consolidation of the industry

As a result of legislation and regulations becoming ever more demanding and complex in Europe and in Belgium, a clear trend in consolidation of chemical distributors in Belgium, being private equity – driven, started in 2005. Mergers and Acquisitions led to eight main players in 2010, with focus on efficiency through inventory management and outsourcing of logistics, and on growth by acquisition. In 2009, external growth strategies for the Belgian market were clearly put on hold, however general consensus is that consolidation will continue, proof of which are acquisitions done by Univar and Azelis in 2010.

On the long term two limitations exist on consolidation in specialty distribution. Firstly, because suppliers require exclusivity, the number of brands existing for a product largely determines the number of distributors in the market. Thus competition in specialties distribution is a direct consequence of competition at the supply side. A second limitation is suggested by the product lifecycle view on chemical distribution: as suppliers carefully select a distributor based on the maturity of their product, they would in many cases refuse to accept consolidation across the lifecycle phases. For example, the acquisition of Kreglinger or Barentz by a firm like Brenntag would urge many principals of the acquired firm to terminate the relationship, because the acquiring firm has a completely different way of interacting with its suppliers (refer to Section 3). Hence the acquisition would actually destroy value. This implication of the product lifecycle view was confirmed by the smaller firms (the potential targets of an acquisition) and they even indicated that their independence is a core condition in their agreements with principals.

6. Conclusions

Based on chemicals trade volumes, the Belgian market is largely dominated by eight major international distributors. Starting from 2010, the market for commodity chemicals is effectively dominated by three firms. For the purpose of describing chemical distribution, the product lifecycle model was found to be a useful tool as many characteristics of firms relate to the phases in the model. Moreover, the product lifecycle view is useful for predicting future consolidation in specialty distribution. In 2009, the year of worldwide economic crisis, distributors were urged to creativity and they developed new business opportunities for their customers and suppliers, leading to a full recovery of the industrial sector in 2010. The European REACH legislation, and the accompanying registration costs, has led to suppliers stepping out of the market for certain chemicals. Chemical distributors fear the possibility of supplier monopoly-formation.

References

Bishop S. & Walker, M. (2010): The Economics of EC Competition Law: Concepts, Application and Measurement, Sweet & Maxwell, London.

CHEManager (2005): Districonsult, Specialty Chemicals Distribution: New Challenges Ahead?

Districonsult, EBDQUIM congres (2010): Chemical Distribution: Outguessing the Year 2020, Sao Paulo.

Districonsult & Solvents Industry Association (2010): European Chemicals Distribution 2010: The Crisis Is Over… What’s Next?, Daventry.

ICIS Chemical Business (2010): Districonsult, The Clouds Part.

ICIS Chemical Business (2010): Guenther Eberhard, Wheels of Change Spin in Distribution, p. 57-58.

VCH (2010): The Chemical Wholesale Trade in Figures: 2009, Cologne.