International M&A transaction volumes along the battery value chain: Strategic investment implications

Abstract

The objective of this study is to examine the international value streams associated with the battery industry, which plays a pivotal role in the global effort to combat climate change. This research provides an in-depth analysis of mergers and acquisitions (M&As) in the global battery market, as a tool for monitoring the innovation strategies of global enterprises in the various regional key markets. Prior research has demonstrated the efficacy of data science methods in the analysis of M&A data across a range of industries and technological domains. An exploratory analysis of a dataset comprising 913 deals from 2018 to 2022 was conducted to investigate the foreign and domestic contributions of North America, Europe, and Asia in relation to individual segments of the value chain. The results highlight North America as the most substantial deal value contributor, peaking in 2021, within the region and investment balance with other key markets. Further, the findings demonstrate that the value streams are largely driven by product manufacturers and enablers.

Keywords: Mergers & Acquisitions; Value chain; Batteries; Data Science; Value stream; Innovation

Introduction

In line with its commitment to achieving carbon neutrality, both society and the global industry have been actively engaged in a long-term process of electrification (Despeisse et al., 2023). The two most significant technological developments are stationary energy storage systems, which facilitate the short-term storage of electricity derived from renewable energy sources, and the ongoing expansion of electric vehicles (EVs), which will ultimately result in a reduction of current emissions from internal combustion engines (ICEs) in the transportation sector (Rísquez Ramos and Ruiz-Gálvez, 2024). Both technologies are based on batteries, particularly lithium-ion batteries (LIBs), which represent a significant cost factor, accounting for approximately one-third of the total cost of an EV (Carlier, 2023). These costs are distributed across the entire value chain, commencing with the extracted powder, and concluding with the implementation in the final application (Bernhart, 2014). This includes the transportation and production of the cells, modules, and packs within gigafactories (Yuan, 2023). A reduction in costs can be pursued through a variety of levers within the value chain, including the reduction of production scrap and the recycling of active materials from used battery packs (Ciez and Whitacre, 2019). Further improvement opportunities arise from the advancement of manufacturing. This incorporates both incremental innovations, which entail the continuous enhancement of process expertise, and radical innovations (Duffner et al., 2021), such as the introduction of dry coating (Ryu et al., 2023). The latter has the potential to serve as a pivotal foundation for the industrialisation of all-solid- state batteries (ASSBs), representing an innovation with the capacity to exert a profound impact on future trends and costs in the context of electrification at the technology level (Randau et al., 2020). In addition to the aforementioned innovations, there are numerous other examples of innovations in the battery industry whose origins are in a state of constant flux (Wang et al., 2023; Xiao et al., 2023).

Research and development (R&D) conducted by companies and academic institutions emerges as a particularly prominent driver (Roper and Hewitt-Dundas, 2013). The reinforcement of R&D and the subsequent enhancement of innovative strength offer a potential competitive advantage for the respective companies or entire regions (Wörter et al., 2010). The consolidation of this growth is achieved, among other means, through the injection of financial incentives, which also include tax reductions and grants (Choi, 2022; Knoll et al., 2021; Mitchell et al., 2020). In the field of battery R&D, such incentives are primarily driven by the respective regional governments with the objective of assisting companies to maintain their relevance within the global value chains (Campagnol et al., 2022; Li et al., 2024; Zhu et al., 2022). Notable examples include initiatives addressing climate change on a global scale, such as the United States’ (US) Inflation Reduction Act and Europe‘s Green Deal, as well as the RISING project in Japan, which is focused on the advancement of novel battery technologies. As a technology leader, China regularly promotes investments allocated to this industry as part of their 5-year plans (Fraunhofer ISI, 2024).

In addition to the examination of government investments in the battery sector, data science methods can be employed to obtain information on technological innovations. In 2024, An and Cho employed bibliographic data to obtain information on international R&D collaborations within the entire battery industry through the application of a network analysis (An and Cho, 2024). In order to obtain an overview of the distribution of expertise along the value chain within a gigafactory cell production, a novel keyword-based patent analysis was also implemented (Greitemeier and Lux, 2024). Despite the growing number of data science-based analyses (Aaldering and Song, 2019; Ahlgren et al., 2023; Hemmelder, 2023; Malhotra et al., 2021), there has been a distinct lack of examination of data from M&As within this context thus far.

M&As represent one aspect of open innovation, facilitating the rapid acquisition of technical knowledge and the generation of productive synergies (Chesbrough, 2010). The application of M&As is categorised as a driver of innovation yet is also subject to critical assessment in other studies. On the one hand, M&As facilitate the expansion of the knowledge base without the necessity for high innovation risks (Cassiman et al., 2005; Cohen and Levinthal, 1990). On the other hand, M&A activity has the potential to weaken competitiveness within the respective industry, which may result in a reduction in research and development (R&D) investments and an impediment to innovation (Hall, 2010). The merits of M&As are a topic of considerable debate in academia. Nevertheless, numerous studies based on M&A data have already been successfully conducted in the fields of agriculture (Hong and Chen, 2022; You and Lio, 2024) and technological expansion (Jin et al., 2024). With regard to the emerging energy industries, Zhu et al. as well as Zhong et al. conducted work to assess the impact of M&As on innovation and performance of enterprises in China, whilst the latter provided a deeper insight into the LIB industry (Zhong et al., 2023; Zhu et al., 2024). The study demonstrated that the number of completed M&As in Chinas LIB industry has increased significantly, from 87 in 2016 to 272 in 2022 (Zhong et al., 2023).

The preceding studies have demonstrated that the analysis of M&A data can provide a deeper understanding of innovation know-how and collaborations within the battery industry. Given the prevailing focus of previous research on the energy sector in China, there is a notable absence of analysis concerning global cooperation through M&As. Moreover, the existing literature has not yet considered the individual value streams separately in the context of M&As. Consequently, this study employs an analytical approach to examine M&A data for a more profound understanding of the global value streams within the battery value chain. Furthermore, the objective is to ascertain the principal regions of each value chain segment, thus facilitating the formulation of strategic implications for investors. This includes the identification of regions that are of vital importance and the way they collaborate on a global scale. Additionally, it entails the determination of value chain segments that represent the most significant targets for M&As and, consequently, innovation. Ultimately, the regional distribution within each segment of the battery value chain is identified.

Materials and Methods

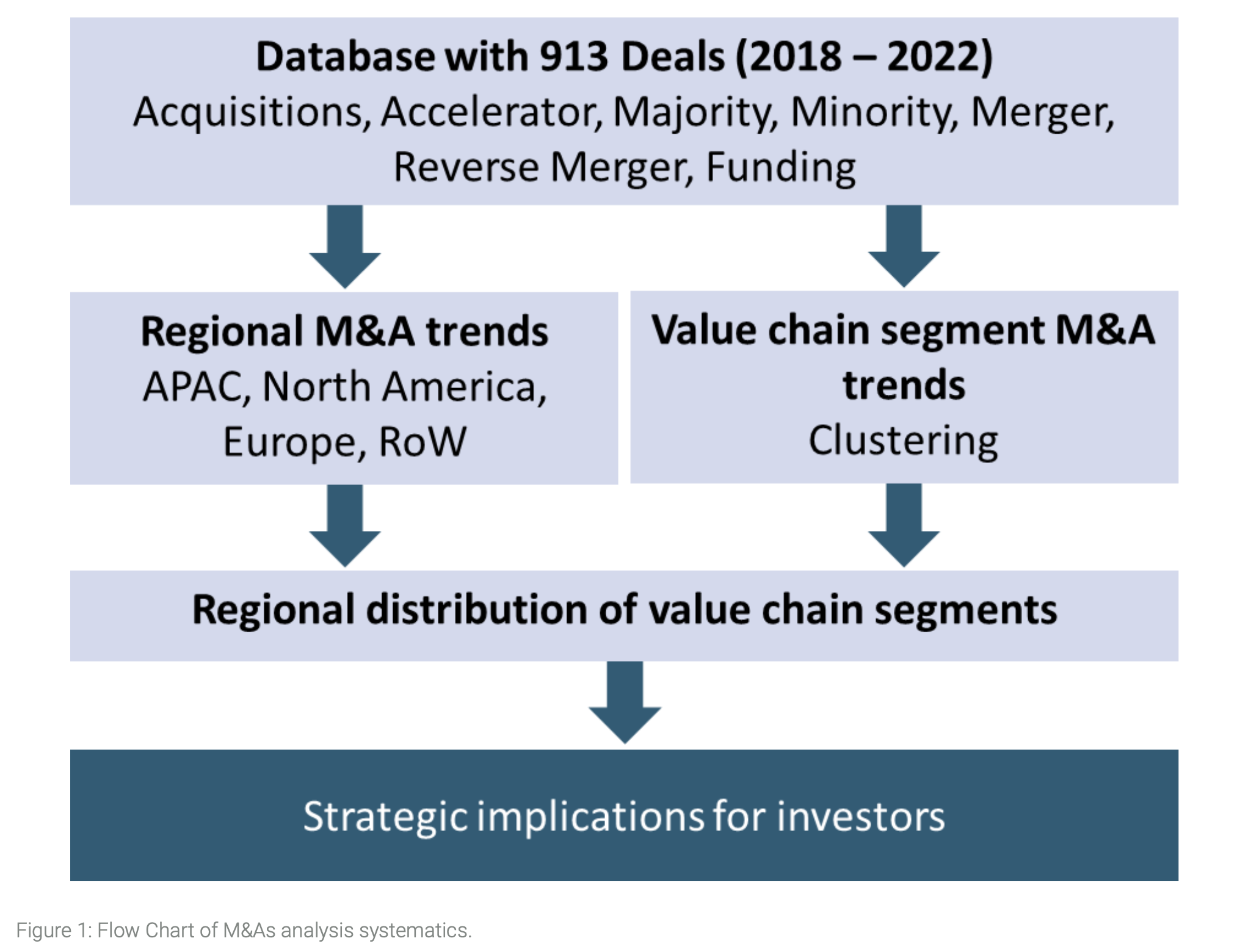

The flow chart proposed for the analysis of M&As consists of three phases of analysis that lead to implications for investors (Fig. 1).

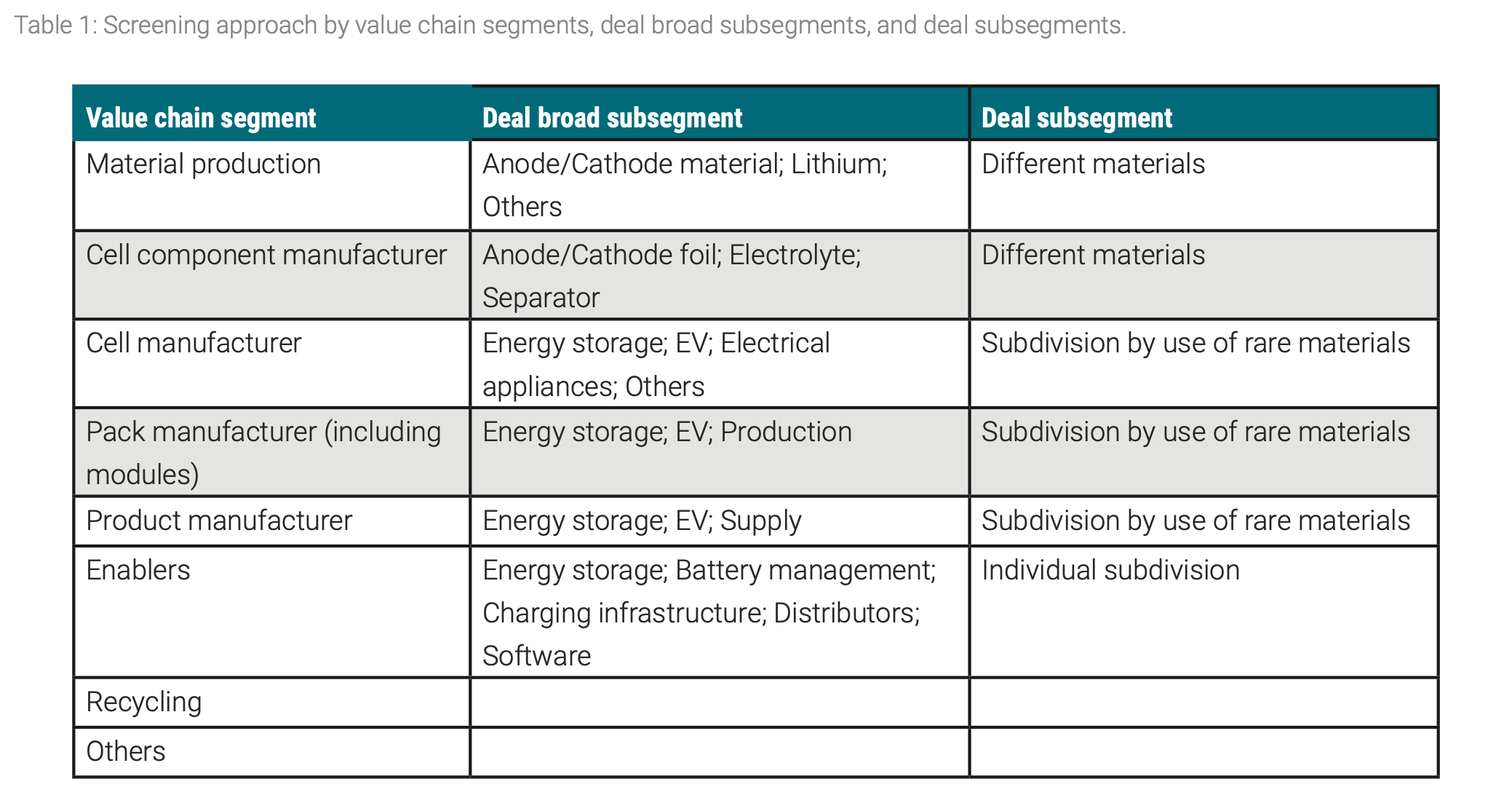

The initial dataset, comprising over 2000 deals, was collected via a combination of public information, pitchbooks and secondary research, including expert interviews. Subsequently, the dataset was reduced to just over 1400 deals. Further exclusion of deals in the renewable energy sector, healthcare, agriculture, and media reduced the dataset to 913 deals. The final dataset of 913 deals was filtered, clustered, and categorized. Categorization was done by adjusting sub-segments (Table 1).

After pre-processing the dataset, the first step is to examine the value flows within and between regions. The analysis period is defined as 2018 to 2022, as M&A deal values significantly increased during this time, but also see some interference due to the COVID-19 pandemic. For the regional breakdown, the three largest competitors, Asia- Pacific (APAC), Europe, and North America, were selected for analysis. The remaining countries are aggregated as the Rest of the World (RoW). The dataset presents business transactions sorted by year and region, allowing examination of regional developments throughout the value chain. In the second phase of analysis, the previously applied categorisation into value chain segments enables the examination of the development of each cluster. The third phase combines the first two phases and is used to assess the geographical distribution of each value chain segment.

Results

Regional M&A trends

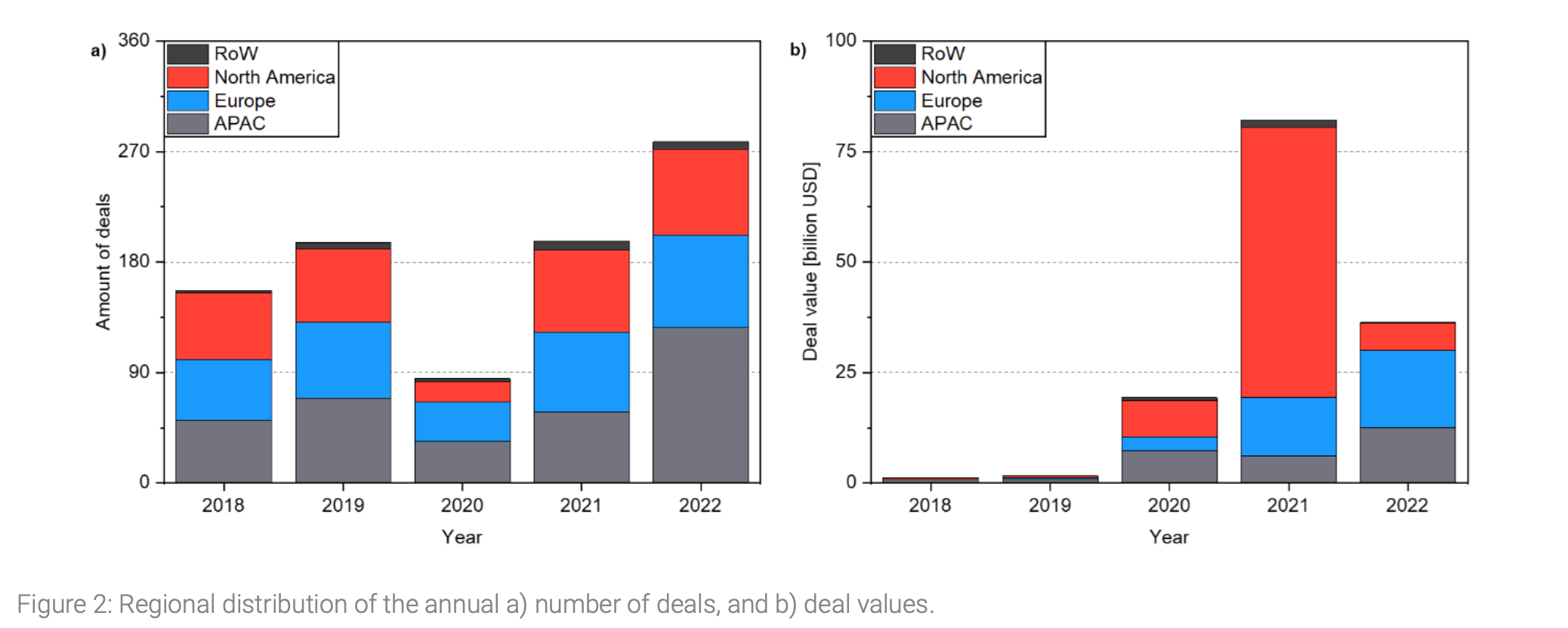

After the final processing the dataset contains 913 deals worth a total of 141 billion US-Dollar (USD). Fig. 2 presents the regional distribution of the annual a) number of deals, and their corresponding b) deal values. Considering the number of deals in a), a steady overall increase from 2018 to 2022 becomes evident, apart from 2020 due to the impact of the COVID-19 pandemic. In 2022, the number of deals reaches a new high of 278, indicating the ongoing rise of the battery industry (Zhao et al., 2021). In this year, APAC has taken the lead with 127 deals, which may indicate a future dominance of this region in the upcoming years. In previous years, the number of deals was evenly distributed across the selected regions, consistently ranging from 50-69, while the RoW reported less than 10 deals each year. In contrast to the amount of deals, the deal values in b) reach their high of 82,098 million USD in 2021, which is dominated by North America with a value share of 74% in this year. The increase of 325% compared to the previous year can be attributed to the occurrence of mega deals, which are defined as deals with a value greater than 3,000 million USD. Although the distribution of deal values was relatively even in 2018 and 2019, it became distorted by several mega-deals in the following years. In 2022, Europe and APAC held the highest value, with North America dropping to third place. The proportion of deal values that are unknown, and which could potentially affect the results, consistently ranged between 13% and 18% throughout the analyzed period. Therefore, this lack of information can be disregarded for the purposes of analysis.

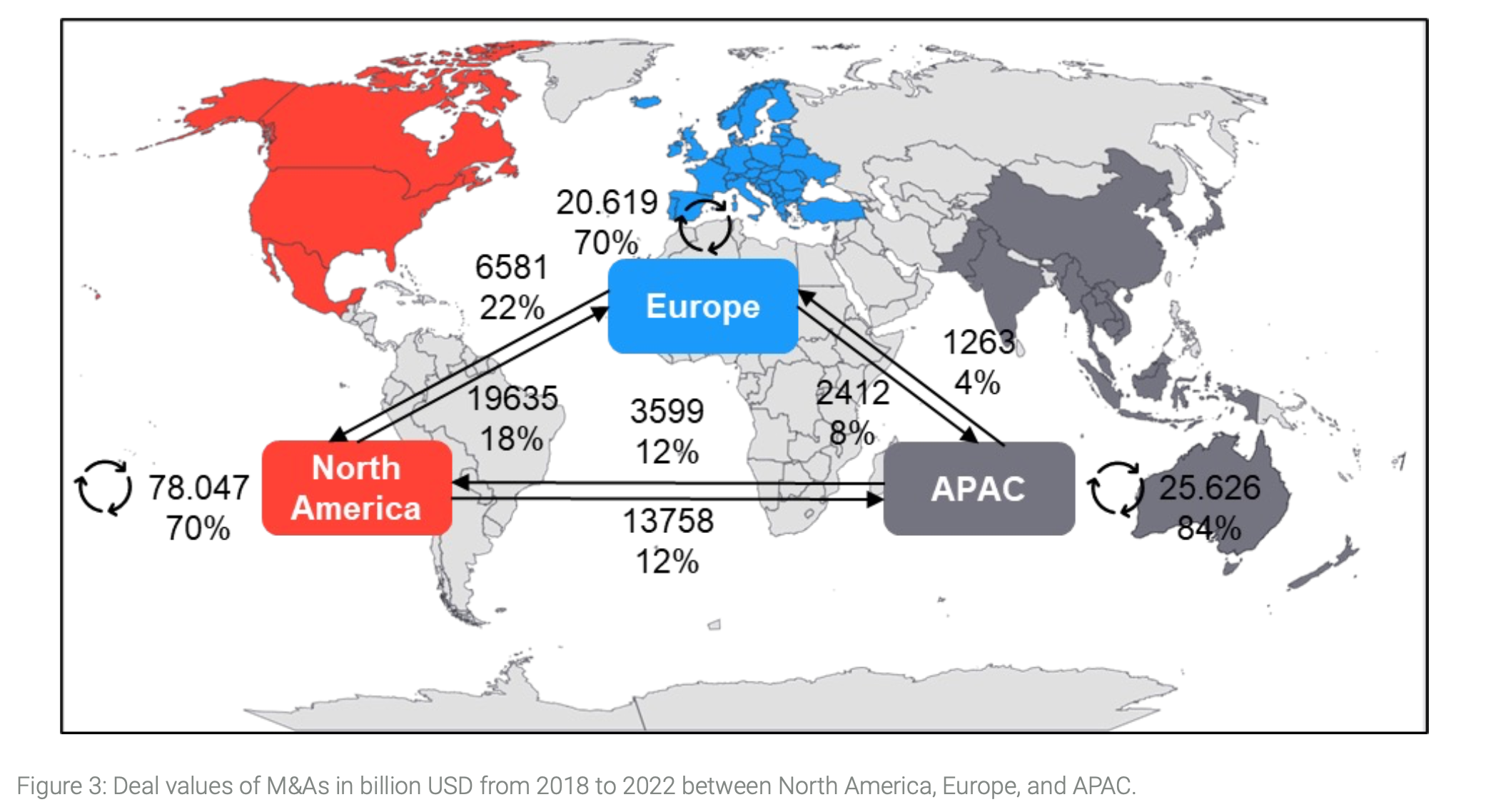

In Fig. 3 the transaction volumes (in millions of USD) between North America, Europe, and APAC in the battery sector from 2018 to 2022 are illustrated. The analysis did not consider the RoW, as their accumulated deal value is only around 2%. North America leads in both domestic and foreign investment, with a total worth of 111,440 million USD. This trend is further reinforced by the IRA, which has given North American companies a sustainable competitive advantage in the US and has driven domestic investments (Bistline et al., 2023; Slowik et al., 2023). Despite the lower deal volumes in Europe and APAC, all three regions primarily focus on domestic investments, with a share above 70%. The APAC region is particularly interested in boosting its domestic markets, with an investment share of 84%, thereby indicating a distinction between APAC and North America and Europe. This trend is also evident in the value of foreign investments, where the connection between Europe and North America sums up to 26,216 million USD, representing a share of 55% of the total foreign investments. As the APAC region, particularly China, Japan, and South Korea, leads the way in battery innovation, the tendency towards domestic investments may suggest a desire to expand their dominance (Beuse et al., 2018; Nedopil, 2023; Stampatori et al., 2020). In this case, it is necessary for North America and Europe to strengthen their position and further expand their connection with the APAC region to increase competitiveness in this booming industry. In certain instances, such as the collaboration between Tesla and Panasonic (Jiang and Lu, 2018), this has already occurred. However, it is crucial to intensify this process in the coming years. Given the intense competition for a competitive market position in the battery sector, this is a matter of critical importance.

Value chain segment M&A trends

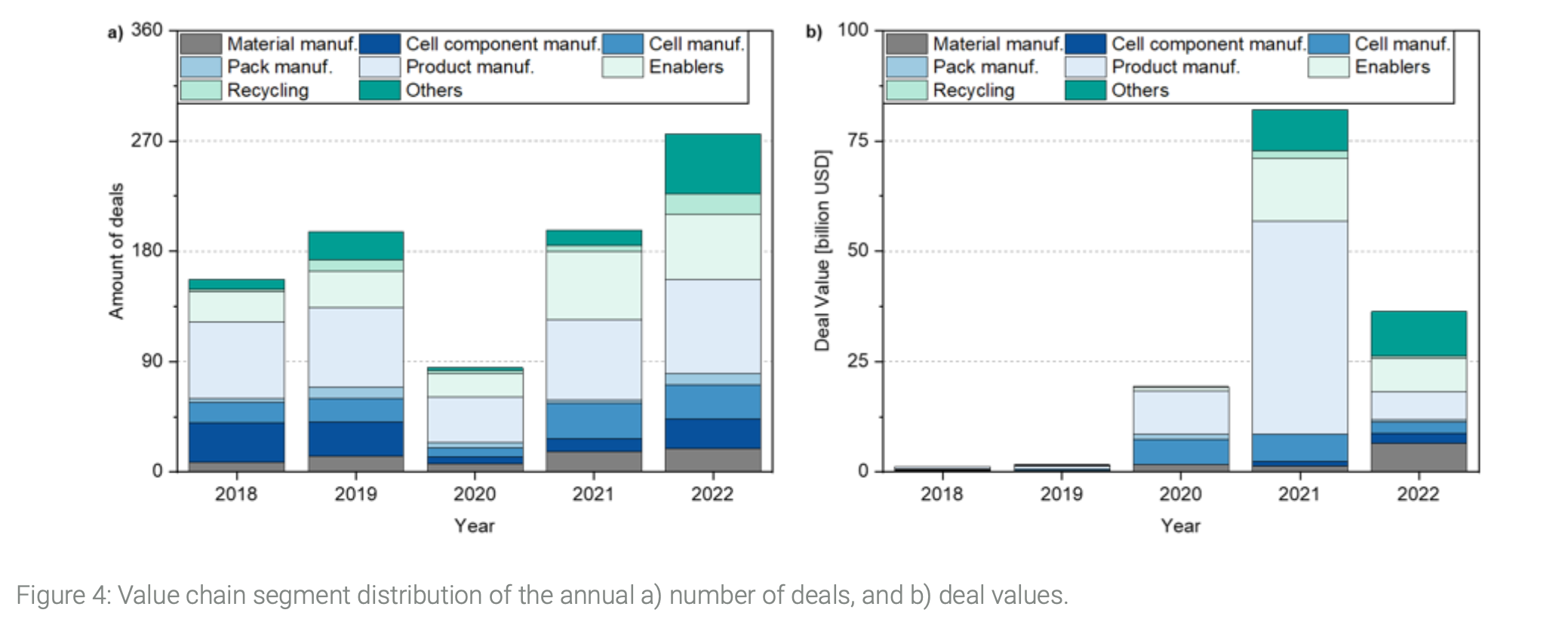

In this part of the study, the annual number of deals and their corresponding deal values are analyzed regarding their value chain segments (Fig. 4). The data in a) indicates that product manufacturers and enablers are the most active deal makers. In 2022, product manufacturers completed a record-breaking 77 deals across all segments, but their growth rate of 24% between 2018 and 2022 is relatively low compared to other segments of the value chain. The recycling segment, which has experienced a growth of 750%, has gained increasing importance over the years. This is consistent with current R&D and policy efforts to expedite the advancement of recycling processes and the transition to circular economy models (Bird et al., 2022).

In the record year 2021, the product manufacturer segment was the main contributor of value, accounting for 59% of the deal values in b). It can be inferred that North American product manufacturers played a significant role in the major deals of 2021. In 2022, the deal values are more evenly distributed, with the segment ‚Others‘ leading with a deal value of 10,145 million USD. As the ‚Others‘ segment includes innovations and trends that do not currently fit into any known cluster, the increase in investment in recent years indicates a growing interest in this sector, which offers many developments in the near future and are maybe outside “classical” segments of the value chain.

Regional distribution of value chain segments

The final step in this analysis is to examine the regional distribution of each value chain segment (Fig. 5). As a consequence of some of the deals being assigned to multiple process steps, the total number of deals and the total value of the deals increased in comparison to the previous results. Both the number of deals and the total deal value are dominated by product manufacturers. The distribution of deals is evenly spread across the top three regions. However, North America has the highest deal values in this segment, suggesting that North American product manufacturers, such as Tesla and a variety of start-up’s, are the most influential in the battery industry (Liu, 2021; Thomas and Maine, 2019). In combination with the previous results, which indicate increasing deal values from North American product manufacturers, it can be deduced that they want to strengthen their position and increase their market share in this segment of the value chain. Overall, it can be inferred that deal activity is highest in Europe across most parts of the battery value chain, but North American manufacturers generate the highest deal values. Currently, the APAC region dominates materials and cell component manufacturing, with companies such as LG Chem, Samsung and CATL leading the world in cell production (Statista Research Department, 2024). When considering the ‚Others‘ segment, which has seen significant growth in recent years, North America is leading the way, particularly in terms of deal values. This success probably can be attributed to the internationally acknowledged R&D in the top universities and the national laboratory system, which pushes innovations in this field (Dutta and Reynoso, 2020).

Conclusion

The study effectively developed a framework to extract strategic insights for investors and policymakers from M&A data in the battery sector. This data facilitated the identification of various trends within the value chain and international competition.

Regional M&A activity analysis reveals that while deals span all regions, North America has generated the highest deal value from both domestic and foreign investments, notably enhanced by the implementation of the IRA. Europe and the APAC region are striving to improve their market positions, evidenced by significant growth in deal numbers and values. The analysis indicates that product manufacturers are the largest contributors to M&A activity, followed by enablers. In 2021, North American product manufacturers dominated the scene, likely completing several mega deals. The rising share of the ‚Others‘ segment suggests advancements and potential innovations outside traditional value chain segments.

The findings indicate a relationship between the North American region and the product manufacturer segment. Additionally, the initial segments of the value chain are primarily led by the APAC region, while the latter segments are deal value leaders in North America.

These insights yield the following strategic implications. First, investors should diversify their investments to mitigate risks and enhance returns. The less prominent value chain segments – pack manufacturing and recycling – present a promising avenue for growth and innovation, particularly recycling due to its increasing necessity. Second, target investment regions differ by segment, as primary production expertise resides in the APAC region, indicating a key market to watch for technology trends. Conversely, the latter segments of the value chain are predominantly in North America, suggesting that investments in the US are favourable for these areas.

However, the study has limitations, including minor inaccuracies in the dataset. For example, there may be discrepancies between listed and operational regions, as company headquarters do not always align with their manufacturing sites. Furthermore, relying exclusively on M&A deals may not fully represent each segment. Future research could incorporate analyses of foreign direct investments to reveal additional deal value trends and provide further insight into the strategic implications. Moreover, this research can be further developed by extending the analysis period and investigating correlations and ratios. This would enable the identification of the underlying rationale behind the deals, which could be achieved by industry interviews.

CRediT authorship contribution statement

Tim Greitemeier: Writing – original draft, Visualization. Simon Lux: Writing – original draft, Supervision. Carina Albrecht: Methodology, Formal analysis, Visualization, Software. Reba Brockington: Methodology, Formal analysis, Visualization, Software. Sebastian Eggers: Methodology, Formal analysis, Visualization, Software. Lars Hansner: Methodology, Formal analysis, Visualization, Software. Niklas Kamp: Methodology, Formal analysis. Hauke Simon: Writing – original draft, Methodology, Formal analysis.

Declarations of interest

None.

References

Aaldering, L.J., Song, C.H., 2019. Tracing the technological development trajectory in post-lithium-ion battery technologies: A patent-based approach. Journal of Cleaner Production 241, 118343.

Ahlgren, P., Jeppsson, T., Stenberg, E., Berg, E., Edström, K., 2023. BATTERY 2030+ and its Research Roadmap: A Bibliometric Analysis. ChemSusChem 16, e202300333.

An, H., Cho, K., 2024. Data Analysis of Global Research Cooperation Patterns in the Secondary Battery Industry. Energies 17, 3030.

Bernhart, W., 2014. The Lithium-Ion Battery Value Chain— Status, Trends and Implications. Lithium-Ion Batteries, 553–565.

Beuse, M., Schmidt, T.S., Wood, V., 2018. A „technology- smart“ battery policy strategy for Europe. Science 361, 1075–1077.

Bird, R., Baum, Z.J., Yu, X., Ma, J., 2022. The Regulatory Environment for Lithium-Ion Battery Recycling. ACS Energy Lett. 7, 736–740.

Bistline, J., Blanford, G., Brown, M., Burtraw, D., Domeshek, M., Farbes, J., Fawcett, A., Hamilton, A., Jenkins, J., Jones, R., King, B., Kolus, H., Larsen, J., Levin, A., Mahajan, M., Marcy, C., Mayfield, E., McFarland, J., McJeon, H., Orvis, R., Patankar, N., Rennert, K., Roney, C., Roy, N., Schivley, G., Steinberg, D., Victor, N., Wenzel, S., Weyant, J., Wiser, R., Yuan, M., Zhao, A., 2023. Emissions and energy impacts of the Inflation Reduction Act. Science 380, 1324–1327.

Campagnol, N., Pfeiffer, A., Tryggestad, C., 2022. Capturing the battery value-chain opportunity.

Carlier, M., 2023. Projected battery costs as a share of large battery electric vehicle costs from 2016 to 2030. https://www.statista.com/statistics/797638/battery-share-of-large-electric-vehicle-cost/. Accessed September 16, 2024.

Cassiman, B., Colombo, M.G., Garrone, P., Veugelers, R., 2005. The impact of M&A on the R&D process: An empirical analysis of the role of technological- and market-relatedness. 0048-7333 34, 195–220.

Chesbrough, H.W., 2010. Open innovation. The new imperative for creating and profiting from technology, [Nachdr.]. Harvard Business School Press, Boston, Mass.

Choi, J., 2022. Do Government Incentives to Promote R&D Increase Private R&D Investment? World Bank Res Obs 37, 204–228.

Ciez, R.E., Whitacre, J.F., 2019. Examining different recycling processes for lithium-ion batteries. Nat Sustain 2, 148–156.

Cohen, W.M., Levinthal, D.A., 1990. Absorptive Capacity: A New Perspective on Learning and Innovation. Administrative Science Quarterly 35, 128.

Despeisse, M., Johansson, B., Bokrantz, J., Braun, G., Chari, A., Chen, X., Fang, Q., González Chávez, C.A., Skoogh, A., Stahre, J., Theradapuzha Mathew, N., Turanoglu Bekar, E., Wang, H., Örtengren, R., 2023. Battery Production Systems: State of the Art and Future Developments, in: Alfnes, E., Romsdal, A., Strandhagen, J.O., Cieminski, G. von, Romero, D. (Eds.), Advances in production management systems. Springer, Cham, pp. 521–535.

Duffner, F., Kronemeyer, N., Tübke, J., Leker, J., Winter, M., Schmuch, R., 2021. Post-lithium-ion battery cell production and its compatibility with lithium-ion cell production infrastructure. Nat Energy 6, 123–134.

Dutta, S., Reynoso, R.-E., 2020. Global innovation index 2020.

Fraunhofer ISI, 2024. Benchmarking International Battery Policies 2024.

Greitemeier, T., Lux, S., 2024. The Intellectual Property Enabling Gigafactory Battery Cell Production: An In-Depth Analysis of International Patenting Trends.

Hall, B.H., 2010. Handbook of The Economics of Innovation. Elsevier Science, Burlington.

Hemmelder, A., 2023. Data-Driven Decision Making in Battery Technology – How to Compete in Global Battery Industry? Meet. Abstr. MA2023-02, 57.

Hong, X., Chen, Q., 2022. Research on the Impact of Merges and Acquisition Type on the Performance of Listed Agricultural Enterprises—An Analysis of Mediator Effect Based on R&D Input. Sustainability 14, 2511.

Jiang, H., Lu, F., 2018. To Be Friends, Not Competitors: A Story Different from Tesla Driving the Chinese Automobile Industry. Manag. Organ. Rev. 14, 491–499.

Jin, G.Z., Leccese, M., Wagman, L., 2024. M&A and technological expansion. Economics Manag Strategy 33, 338–359.

Knoll, B., Riedel, N., Schwab, T., Todtenhaupt, M., Voget, J., 2021. Cross-border effects of R&D tax incentives. 0048-7333 50, 104326.

Li, Z., Pang, S., Shen, X., 2024. Effects of non-subsidized industrial policies on embedding position of power lithium- ion battery manufacturers in global value chain: Firm level evidence from China. Journal of Cleaner Production 461, 142681.

Liu, S., 2021. Competition and Valuation: A Case Study of Tesla Motors. IOP Conf. Ser.: Earth Environ. Sci. 692, 22103.

Malhotra, A., Zhang, H., Beuse, M., Schmidt, T., 2021. How do new use environments influence a technology‘s knowledge trajectory? A patent citation network analysis of lithium-ion battery technology. 0048-7333 50, 104318.

Mitchell, J., Testa, G., Sanchez Martinez, M., Cunningham, P.N., Szkuta, K., 2020. Tax incentives for R&D: supporting innovative scale-ups? Res Eval 29, 121–134.

Nedopil, C., 2023. China Belt and Road Initiative (BRI) Investment Report 2021.

Rísquez Ramos, M., Ruiz-Gálvez, M.E., 2024. The transformation of the automotive industry toward electrification and its impact on global value chains: Inter- plant competition, employment, and supply chains. 2444-8834 30, 100242.

Roper, S., Hewitt-Dundas, N., 2013. Catalysing open innovation through publicly-funded R&D: A comparison of university and company-based research centres. International Small Business Journal 31, 275–295.

Ryu, M., Hong, Y.-K., Lee, S.-Y., Park, J.H., 2023. Ultrahigh loading dry-process for solvent-free lithium-ion battery electrode fabrication. Nat Commun 14, 1316.

Slowik, P., Searie, S., Basma, H., Miller, J., 2023. Analyzing the impact of the Inflation Reduction Act on electric vehicle uptake in the United States.

Stampatori, D., Raimondi, P.P., Noussan, M., 2020. Li-Ion Batteries: A Review of a Key Technology for Transport Decarbonization. Energies 13, 2638.

Statista Research Department, 2024. Global market distribution of lithium-ion battery makers in 2023. https://www.statista.com/statistics/235323/lithium-batteries-top-manufacturers/. Accessed September 16, 2024.

Thomas, V.J., Maine, E., 2019. Market entry strategies for electric vehicle start-ups in the automotive industry – Lessons from Tesla Motors. Journal of Cleaner Production 235, 653–663.

Wang, H., Dai, J., Wei, H., Lu, Q., 2023. Understanding technological innovation and evolution of energy storage in China: Spatial differentiation of innovations in lithium-ion battery industry.

Wörter, M., Rammer, C., Arvanitis, S., 2010. Innovation, Competition and Incentives for R&D.

Xiao, J., Shi, F., Glossmann, T., Burnett, C., Liu, Z., 2023. From laboratory innovations to materials manufacturing for lithium-based batteries.

You, Y., Lio, C., 2024. Characteristics and Economic Consequences of Mergers and Acquisitions in China’ s High-tech Enterprises under the Wave of Agricultural M&A. Journal of Yunnan Agricultural University 18, 54–62.

Yuan, C., 2023. Sustainable battery manufacturing in the future. Nat Energy 8, 1180–1181.

Zhao, Y., Pohl, O., Bhatt, A.I., Collis, G.E., Mahon, P.J., Rüther, T., Hollenkamp, A.F., 2021. A Review on Battery Market Trends, Second-Life Reuse, and Recycling. Sustainable Chemistry 2, 167–205.

Zhong, J., Chun, W., Deng, W., Gao, H., 2023. Can Mergers and Acquisitions Promote Technological Innovation in the New Energy Industry? An Empirical Analysis Based on China’s Lithium Battery Industry. Sustainability 15, 12136.

Zhu, L., Shen, J., Yeerken, A., 2024. Impact analysis of mergers and acquisitions on the performance of China‘s new energy industries. Energy Economics 129, 107189.

Zhu, X., Liu, K., Liu, J., an Yan, 2022. Is government R&D subsidy good for BEV supply chain? The challenge from downstream competition. Computers & Industrial Engineering 165, 107951.